Clearly, FinTech has caught on around the world and we expect that new players and services will emerge in the future. But the only question is how to earn a position in the market and make it completely unique and not a copycat. Careful planning and preparation are the keys to a successful business. Here is an overview of 5 important steps you need to take when starting a fintech company:

ANALYSE TYPES OF INSTITUTIONS AND REGULATIONS CAREFULLY

In order to start a fintech company, first, you need to study and be familiar with the difference between various types of financial institutions.

Electronic money institution (EMI) vs Payment institution (PI) – what to choose

If you are planning to provide a variety of payment services in Europe – you will need to get an Electronic Money Institution (EMI) or Payment Institution (PI) license. The major difference between these two licenses is that with the EMI, in addition to payment services, you will be able to issue electronic money.

For each license, there are minimum initial capital requirements, e.g., for PI from EUR 20 000 (money remittance only) to EUR 125 000, for EMI from 350 000. The EMI license is more expensive and suitable for bigger companies, who are looking to invest in fintech and establish partnerships with more solid banks and other industry players.

For start-ups with limited financing, small PIs or EMIs are a better fit. There are limitations for turnover – average monthly payment transactions in the preceding 12 months must not exceed EUR 3 million. Just keep in mind that you can start with a small PI or EMI and then upgrade to a more sophisticated institution.

You should consider that there are plenty of laws, regulations, and restrictions governing the rights of a fintech business and these requirements differ from country to country.

Jurisdictions – how to choose

So, which European countries are represented on the list of the most promising destinations to start a fintech company? As we all know a European financial centre is based in London, therefore the biggest part of all EMI & PI licenses in Europe are clustered in the UK. Lithuania is the second popular regulator because operational expenses are lower and business conditions – more favourable. Malta and Cyprus came next in the ranking.

Other jurisdictions are more challenging. Some of them have strict requirements to apply for a license that involve equity capital, shareholders, and company management. In some jurisdictions, there are regulations that can cause you difficulties in opening a current account in local banks. Some are very expensive and time-consuming. To clarify all the facets and nuances of regulators, Advapay is happy to help and discuss everything in a private meeting.

CHOOSE YOUR NICHE

In any case, to enter a new industry and start a fintech company, it is important to conduct research and analyse the market, competitors, and consumers.

Online banking solutions, money remittance, payment processing – there are different categories of fintech services. To be competitive, choose your niche and identify your target audience. Think about what new products or services can be developed or analyse what problems customers face.

Once you define your product and services, the market analysis will be very helpful in developing your Unique Selling Point (USP). Every unique product or innovation that offers something different and disrupts the market successfully has always been the one that stands at the forefront of the competition. As there are many fintech companies and the industry is getting crowded, the importance of innovation and developing new solutions has never been more substantial.

MAKE PARTNERSHIPS

Unfortunately, obtaining a license is only half the battle. Fintech platforms aren’t stand-alone services but require partnerships with other industry players. You will need partners from the very start to be successful. So, when considering partners, we suggest looking for experienced legal and business consultants, who are experts in the field and they have done this before.

Many lawyer firms offer fintech newbies services to prepare documents for licensing, but be aware that they will prepare only legal documents. Meanwhile, companies with expertise in payment technologies and infrastructures can provide all-inclusive services, e.g., guidance on licensing and starting a business, operational policies, a segregated account in a bank for customers’ funds, etc.

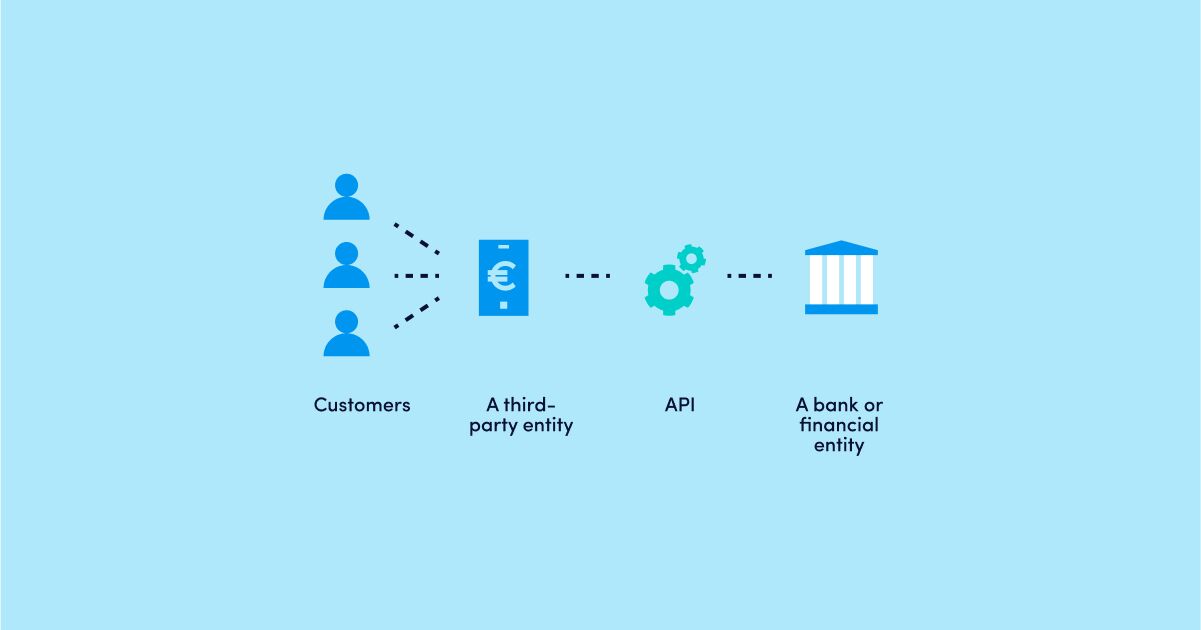

To start a fintech business, you need to be connected to different banks, acquirers, FX, payment cards issuers, money transfer systems, payment processing and clearing systems, SWIFT, and SEPA, etc. You will have to think about opening safeguarding accounts for customers’ funds in several banks. This task seems very simple, but without a reliable partner, it will be a huge challenge. In addition, a competitive fintech company provides value-added services, such as the issuance of co-branded card and acquiring. And the main priority and the most important task – you will need to evaluate and select a software provider for your fintech platform. Advapay offers all these services to connect you to a fintech engine.

CALCULATE AND RAISE THE NECESSARY CAPITAL

A fintech start-up isn’t cheap and you need to make sure you are financially ready to start a company.

Let’s face it, first, you need to do a little homework and write a business plan – it will help your fintech start-up get organized. Do not hesitate to ask for help from experts to write a good business plan. Keep in mind that regulators require financial forecasts for the next 3 years.

If you don’t establish a joint venture with a financial service firm or any other investor, who has financial resources to develop a product, then be prepared to spend a huge amount of time and money to get skilled people on board. Fintech companies are facing the competition because traditional banks try to get the best pool of talents for themselves.

Starting your fintech business means you need to consider capitalization volume in the first years. Operating expenses can increase due to rapid business extension and new partnerships with new third-party providers (TPPs).

Ongoing capital

Another issue is an ongoing capital. This is one of the most frequently asked questions. Can I use money of the initial capital for running the company, software and business development? Yes, you can. But you need to know your ongoing capital – the amount beyond which you cannot go. The calculation of the ongoing capital should be submitted annually as a report to your regulator. If you miss it – you can lose your license.

GET YOUR SYSTEM READY AND START MAKING MONEY

The next step to start a fintech company – is your IT system. Once you have applied for a license and paid the initial capital, you will have to develop a fintech platform, hire your team and open your office. On average, you will need about 3-6 months to receive the license. During this stage, you need to have a clear strategy about implementing either SaaS services or a system on your side.

Let`s compare two options – there are pros and cons of having a system implemented on your side (software license) and Software as a Service (SaaS). Switching to Software as a service (SaaS) will be 2-3 times cheaper than internally implemented services and you will be able to get the system running in less than 2 months. This solution will be more suitable for small companies that are looking to get off the ground fast without making huge investments.

Whereas a full license grants extensive functionalities to serve bigger customer portfolios and brings unlimited options for designing a solution on-demand. You will be able to customise your services as soon as your business grows.

When you choose your platform, think of the functionalities that are popular among competitors and potential clients. For example, VISA or Mastercard acquiring and issuing, SWIFT and SEPA payments, IBAN for customers and other functionalities that can help you effectively sell your services and attract new clients to your fintech platform.

It sounds impossible, but not with us. To make your first steps in fintech hassle-free, Advapay is here to help you!

Good luck!

Advapay is a technology company providing the Digital Core Banking platform to empower fintech clients or digital banks to start their businesses and accelerate digital transformation. The platform delivers all essential functionalities, a front-to-back system and a set of tools to customise and bring new integrations. With Advapay, potential and existing customers can connect either to the cloud-based SaaS or on-premise software. Besides the technical infrastructure, the company provides business advisory and fintech licensing services. Interested to learn more, please drop us a message.