Директива о платежных услугах (PSD), а позже вторая директива о платежных услугах (PSD2) — это директивы Европейского союза (ЕС), которые были разработана для регулирования платежных услуг и поставщиков платежных услуг в Европейском союзе (ЕС) и Европейском экономическом пространстве (ЕЭЗ).

В 2009 году, когда была введена правовая основа единого платежа для еврозоны (SEPA), Европейский Союз принял Директиву о платежных услугах PSD.

Что изменилось с приходом PSD2?

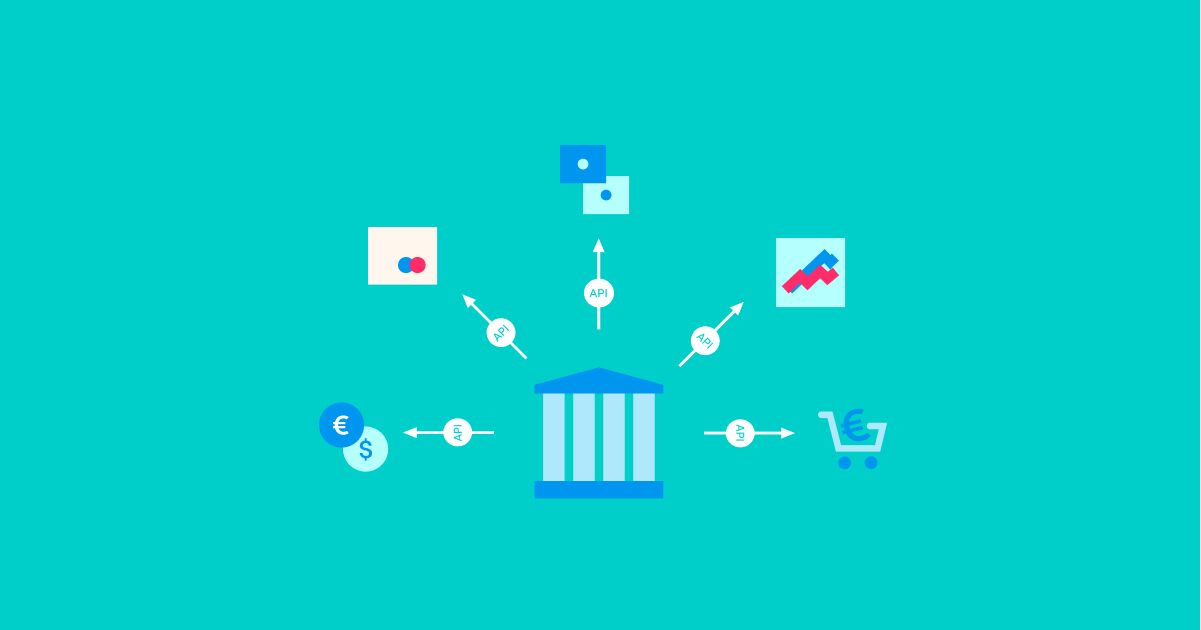

Из-за растущего числа финтех-компаний в финансовой индустрии, в 2016 году вступила новая, пересмотренная вторая директива о платежных услугах (PSD2), которая принесла с собой Открытый банкинг (Open Banking). Открытый банкинг – это комплекс решений и процессов, позволяющий банкам и сторонним поставщикам услуг (TPP) надежно обмениваться финансовой информацией и услугами в электронном виде и с разрешения клиентов. Дополнительно, директива привнесла изменения и в аутентификацию клиентов, предписывая требования для внедрения строгой аутентификации клиентов (англ. Strong Customer Authentication, SCA), которая сделает онлайн-транзакции более безопасными и уменьшит мошенничество с платежами. Время внедрения SCA было отложено из-за неготовности индустрии и Европейский банковский орган продлил окончательный срок внедрения до декабря 2020 года.

Необходимость и цель второй директивы о платежных услугах PSD2

Вторая директива о платежных услугах PSD2 была создана, чтобы сделать платежи в Европейском Союзе более эффективными и безопасными. Новая директива направлена на продвижение инноваций и повышение защиты потребителей и безопасности платежей.

Common and secure communication (CSC) является еще одним важным компонентом PSD2. Услуги электронной идентификации и доверия (англ. Electronic Identification and Trust Services, eIDAS) являются нормативными стандартами для онлайн-транзакций в Европейском Союзе (ЕС). Цифровые сертификаты, определенные eIDAS, используются для идентификации и проверки банков и провайдера платежных услуг (PSP), шифрования сообщений и предоставления электронных печатей для транзакций и данных, передаваемых между различными финансовыми учреждениями. PSD2 направлена на развитие единой интегрированной индустрии платежей, которая имеет стандартизированные директивы о том, как работают банки и другие поставщики платежных услуг. Кроме того, PSD2 обеспечивает подотчетность и честную конкуренцию, поскольку регулирование снижает барьеры для доступа сторонних поставщиков.

Macrobank – платформа цифрового банкинга, которая позволяет финтех-компаниям запускать свои цифровые банки. Macrobank обеспечивает все необходимые функции для цифровых банков, бэк-офис для контроля и управления операциями, веб и мобильные аппликации для конечных пользователей по модели white-label, а также готовые интеграции с различными сервисами. Доступно как SaaS решение, так и покупка лицензии на программное обеспечение.

Помимо платформы Цифрового банкинга, услуги Advapay включают в себя профессиональный финтех консалтинг, помощь в лицензировании платежных систем или эмитентов электронных денег.

Свяжитесь с нами сегодня, чтобы узнать, как Advapay может помочь вам начать свою финтех-компанию.