Developing your Core Banking and other applications usually requires considerable time and financial investment. Instead of building your own Core banking, fintechs can implement white-label banking solutions to minimise time-to-market and save resources.

In the article, we will address white-label banking and its benefits. It will help to understand better whether white-label banking would be the right solution for your fintech company to get ahead of the curve.

What is white-label banking?

White-label banking is the core and a pre-packaged range of ready-made components. White-label solutions comprise prebuilt modules and integrations or APIs to connect to external service providers, but it is also possible to develop new branded services without creating them from scratch.

White-label banking products

With a variety of different white-label banking services, you will be able to embed all various features into your proposition:

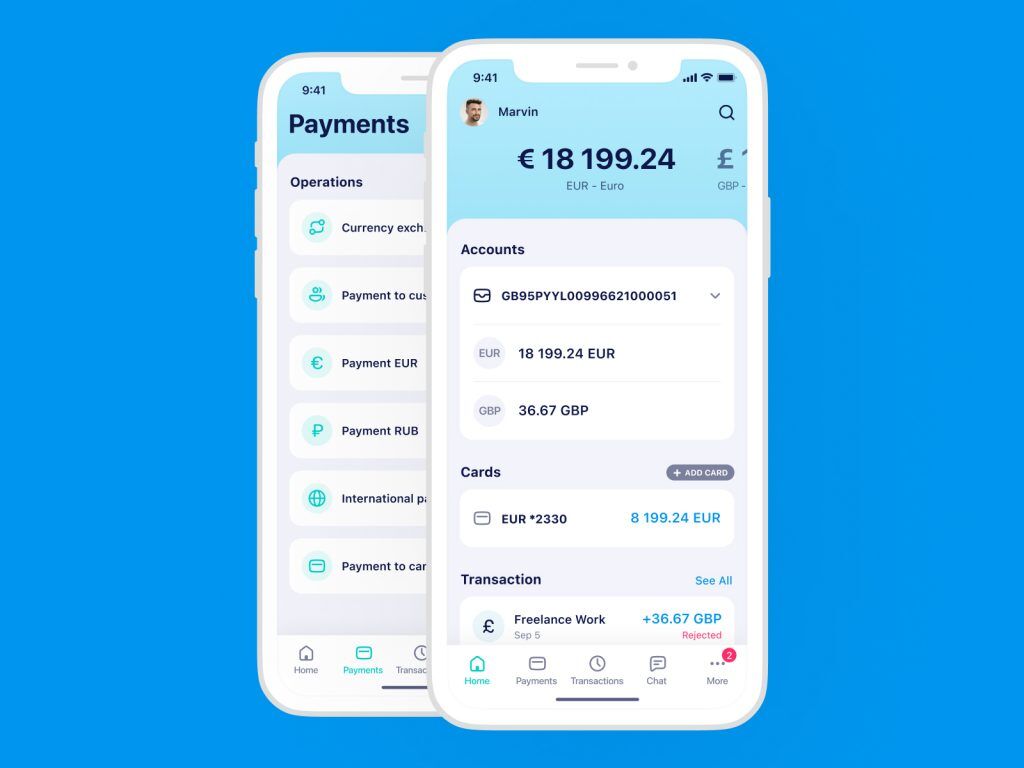

Client onboarding, AML/KYC: When new clients sign up on your platform, they will be required to follow through the onboarding process to set up an account and provide relevant information. KYC/AML functionality will help to establish customer identity and ensure that customer data are verified against different databases, while providing an effortless experience for end-users.

Payments & Currency exchange: building a payment network is one of the most complicated challenges, but with ready-to-use white-label payment & FX services, you will be able to connect to the extended payment infrastructure and provide your customers with different payment methods and currencies.

License-as-a-Service: With a white-label banking solution, you can build your products like blocks. One of these blocks is a license-as-a-service, meaning that fintechs can operate under 3rd parties’ EMI, PI, and Bank licenses.

Debit card issuance: with the proper integration provided by a card issuing supplier, you can issue debit cards to users through a web bank or mobile banking application.

IBAN sponsorship / Virtual IBANs: There are dozens of regulated e-money companies that offer the opportunity to generate IBANs without the need for an individual e-money or payment license and joining a SEPA scheme. Such companies allow to issue and manage IBANs automatically through their API. These IBANs are created in the partner’s name – the customer receives a dedicated IBAN with partner (e.g., bank, payment system) details.

It is possible but very complicated to integrate white-label solutions from different providers on your own. Advapay is here to help you to integrate various features on a ready-made platform with a specially designated integration hub, which means that you will incorporate all the necessary functionalities and services to launch your fintech business.

White-label banking applications vs white-label banking

White-label banking is more related to back-office operations and a banking engine. White-label banking applications are end-user applications, like web bank or internet bank and a mobile app. They can well complement white-label banking and work as one solution.

White-label applications allow fintech companies to develop a complete suite of branded applications without huge investments. As a result, extensive features can be deployed, providing a smooth user experience in the shortest possible timeframe.

What are benefits of white-label banking?

Many fintech companies prefer to partner with white-label banking providers. There are many benefits of building your fintech applications using APIs provided by banking-as-a-service companies:

Save resources:

Alternatively, you can develop your solution from the ground up. However, it will require an experienced internal team and human resources to code and develop. Then, it will be essential to test and fix bugs. All in all, you will need to invest a massive amount of money. Instead, you can outsource the whole process to cut expenses and the timeframe to get it done.

Benefit from experts:

White-label providers usually offer solutions that integrate a mix of the latest technologies thoroughly tested and align with regulatory requirements of the fintech world.

Get to market faster:

Why not skip the time-consuming application development and testing phase? With white-label solutions, you will be able to market quicker and add new functionalities to your core just like that without spending much time on creating them from scratch. Then, the only thing you need to do is to configure solutions and start selling them.

Know your product from the very start and use it:

Get acquainted with your product – test, touch it and start using it. There will be many unexpected events when you build the applications on your own. The fintech industry is changing rapidly, but the product development process can be 1-2 years long. For this reason, your new release may be outdated and come to the market too late.

Know your budget from the start:

You can precisely calculate your expenses to start a fintech business or make some additions. White-label solutions vendors, like Advapay, offer clear packages depending on each module and integration. However, fintech companies usually delay their project timeline, and actual expenses go over the budget in the case of an in-house solution.

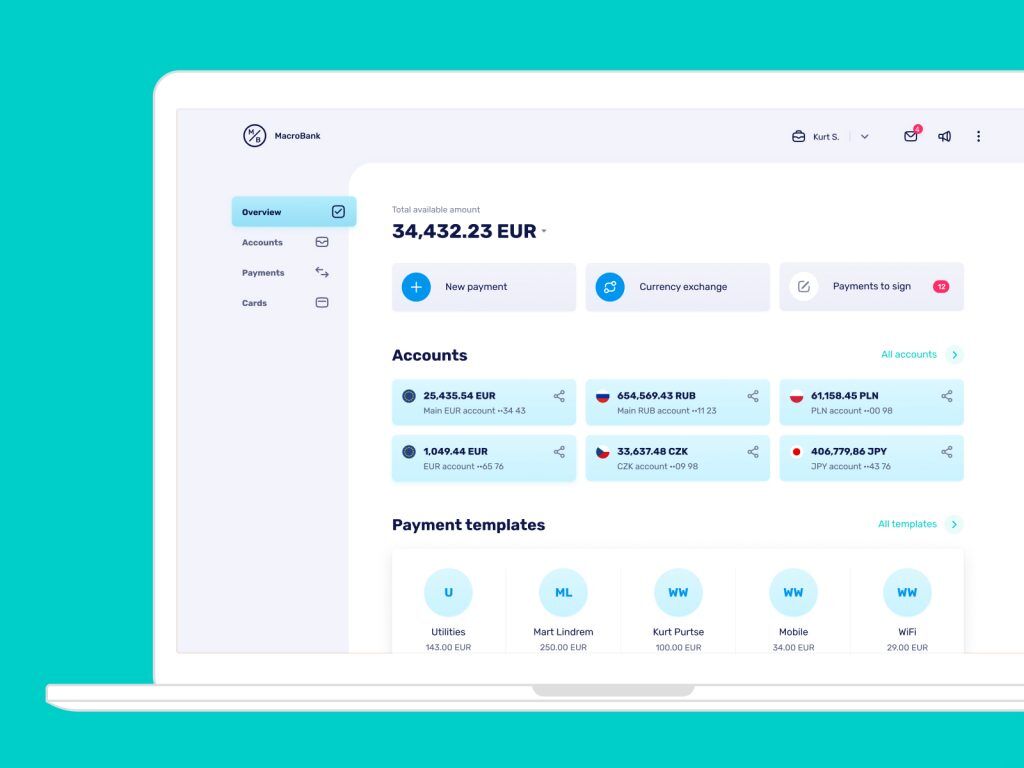

White-label digital banking solution Macrobank by Advapay allows fintech companies to get their products to market faster and benefit from tools developed by our experts. Have a lot of questions in your mind about White-label banking? Contact us to learn more.