Sometimes the quest to find the best digital core banking platform requires an understanding of your business needs and other relevant factors, including a digital strategy and budget, technical capabilities, an implementation timeframe, standards and experience of providers (on both a local and global scale), solution strategy and an action plan, etc.

This blog post explores the main criteria are required for the platform to help digital banks and fintechs cost-effectively increase the competitive advantage.

1. Future-proof microservice architecture

In the digital era, the personalised approach comes down to a set of technologies and the capacity to quickly develop and implement new functionalities and features. This is where a microservice architecture plays an important role and helps digital banking businesses to increase flexibility and to enable them to transform their businesses fast.

A digital banking platform based on a microservice architecture is especially helpful in developing new functionalities, integrations, making changes or customisations. This type of architecture brings innovations to a completely new level, because businesses can use their own technologies to quickly develop new services or extend the existing.

2. Fast-to-market digital banking platform

Fintech companies must be agile and flexible in responding to ever-changing customer demands and market changes. It means that they must be able to quickly launch digital financial products and services and make modifications whenever it is needed.

At the start your digital banking platform must offer all main functionalities, including customer onboarding and AML/KYC, current accounts, payment processing, accounting, etc, as well as to support fast delivery time for implementation or any upgrades and changes.

For the first phase, integrate SaaS, as a ready-to-go solution with predefined functionality. There are only limited possibilities to extend the functionality – you will only be able to choose features from the list provided by the provider. Later on, when you need to make your product unique or just you have an increased customer number, our team recommends you to transit to the software license. This will enable you to add more complex digital banking features easily, connect new payment solution providers, and much more.

Another point to be mentioned is that the Core Banking platform must offer white-label front office – web and mobile applications for consumers. Development of your own solutions for front-office can take at least six months and such a long period is inacceptable to enter the market. But if you connect, rebrand and customise ready-made apps, you will be able to offer new services to your customers immediately.

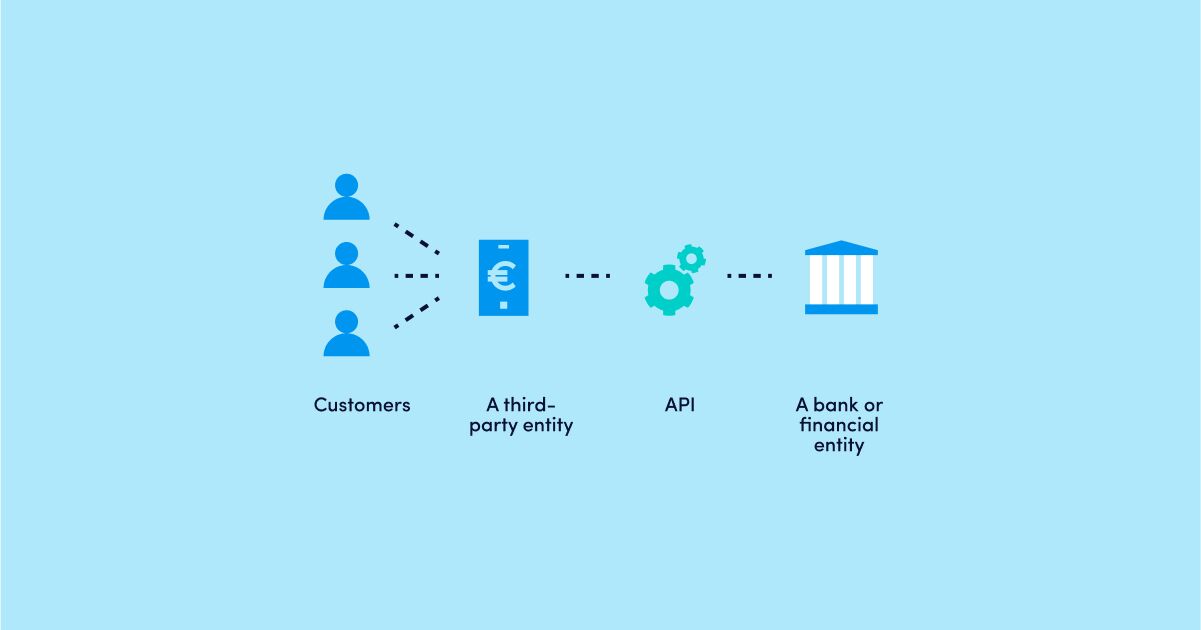

3. Open banking readiness

Open Banking is a part of a sweeping piece of European legislation known as the second Payment Services Directive, or PSD2 and it is no longer in question, especially in Europe. Your open banking strategy is an important factor in making a decision which digital banking platform would best to integrate.

All-in-one fintech solutions and applications become popular as they deliver great value for consumers. With open APIs, you can easily integrate third parties and other banks with your ecosystem and make new, value-added products available to your customers that are otherwise impossible to implement. With the help of open API, digital banks can offer additional products, for example, insurance, loyalty, personal finance management, and connection to any other service.

Above all, the open banking strategy can turn the existing solution into new revenue streams while providing data access for third-party providers.

4. Ready-to-use and ready-to-implement integrations with service providers

An end-to-end digital banking platform is not just an engine, front and back-offices, but it is a complex system with connections to different service providers. With more and more service providers offered by the digital banking platform, there are more and more functionalities available. Fintechs can avail services of such providers as banks, currency exchange providers, AML/KYC providers, remittance and different payment systems. Having this in mind, the digital banking system must offer in-built integrations and support technically any additional integrations your business needs.

A flexible infrastructure and integration framework are the key to ensure business continuity and increase the competitive advantage of any digital bank. In practical terms, the integration framework interconnects your business units and increases efficiency, whereas flexibility of your infrastructure means that you can focus on your business growth and continuously work on new development.

Advapay is a technology company providing the Digital Core Banking platform to empower fintech clients or digital banks to start their businesses and accelerate digital transformation. The platform delivers all essential functionalities, a front-to-back system and a set of tools to customise and bring new integrations. With Advapay, potential and existing customers can connect either to the cloud-based SaaS or on-premise software. Besides the technical infrastructure, the company provides business advisory and fintech licensing services. Interested to learn more, please drop us a message.